Bhushan Ekbote · April 18, 2026

The Training Rule

I was on a call last week with an owner who told me his team "just doesn't get it."

I asked him to walk me through how he trained them.

He paused. Then he said, "Well, I showed them once. And I answered their questions when they had them."

That was it. One time. Maybe some Q&A.

And now he's frustrated that they're doing it wrong, doing it slowly, or coming back to him for every decision.

Here's what I've come to call the Training Rule: you don't have a people problem, you have a process problem. And most process problems trace back to a training problem.

When you train someone once, you're not really training them. You're introducing them to a concept and hoping it sticks. Real training is repetition, feedback, correction, and confirmation. It's checking whether the person can do the task without you, not just whether they sat through your explanation.

Most owners skip this because it feels slow. They'd rather just do the thing themselves. And in the short term, that works. But six months later, they're still doing the thing themselves, still frustrated, still convinced their team can't handle it.

The business doesn't grow because the owner never actually let go. And the owner never let go because the training never actually happened.

If your team keeps getting it wrong, or keeps coming back to you, ask yourself honestly: did you train them, or did you just tell them once?

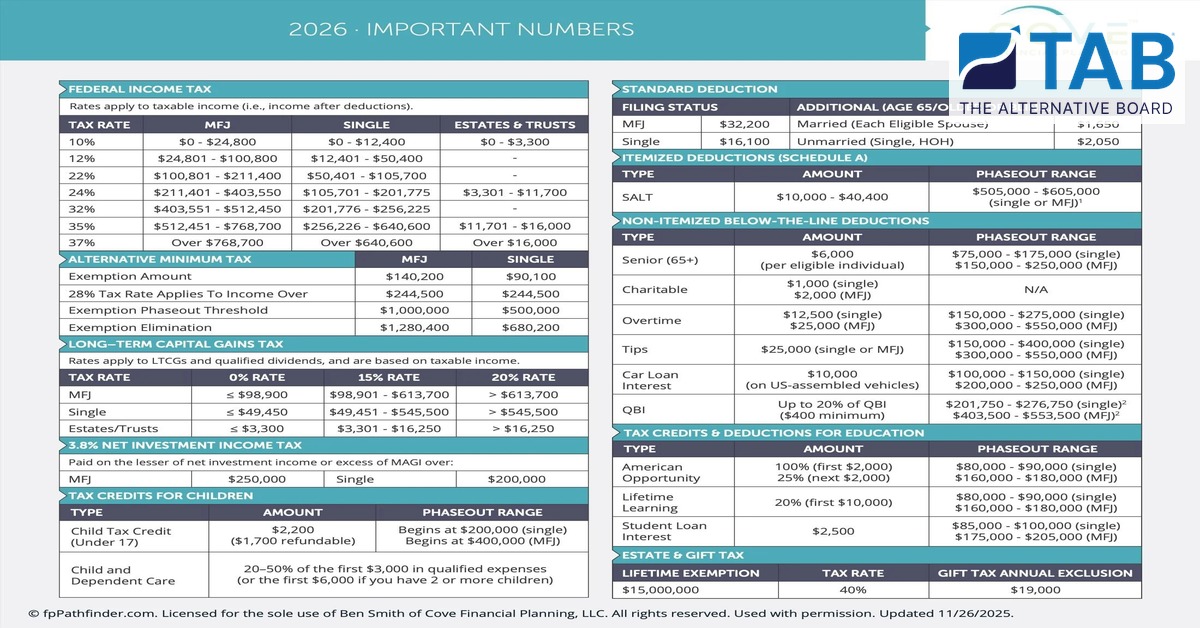

2026 · IMPORTANT NUMBERS

| FEDERAL INCOME TAX |

|---|

| Rates apply to taxable income (i.e., income after deductions). |

| TAX RATE | MFJ | SINGLE | ESTATES & TRUSTS |

|---|---|---|---|

| 10% | $0 - $24,800 | $0 - $12,400 | $0 - $3,300 |

| 12% | $24,801 - $100,800 | $12,401 - $50,400 | - |

| 22% | $100,801 - $211,400 | $50,401 - $105,700 | - |

| 24% | $211,401 - $403,550 | $105,701 - $201,775 | $3,301 - $11,700 |

| 32% | $403,551 - $512,450 | $201,776 - $256,225 | - |

| 35% | $512,451 - $768,700 | $256,226 - $640,600 | $11,701 - $16,000 |

| 37% | Over $768,700 | Over $640,600 | Over $16,000 |

| ALTERNATIVE MINIMUM TAX | MFJ | SINGLE |

|---|---|---|

| Exemption Amount | $140,200 | $90,100 |

| 28% Tax Rate Applies To Income Over | $244,500 | $244,500 |

| Exemption Phaseout Threshold | $1,000,000 | $500,000 |

| Exemption Elimination | $1,280,400 | $680,200 |

| LONG-TERM CAPITAL GAINS TAX |

|---|

| Rates apply to LTCGs and qualified dividends, and are based on taxable income. |

| TAX RATE | 0% RATE | 15% RATE | 20% RATE |

|---|---|---|---|

| MFJ | ≤ $98,900 | $98,901 - $613,700 | > $613,700 |

| Single | ≤ $49,450 | $49,451 - $545,500 | > $545,500 |

| Estates/Trusts | ≤ $3,300 | $3,301 - $16,250 | > $16,250 |

| 3.8% NET INVESTMENT INCOME TAX | |

|---|---|

| Paid on the lesser of net investment income or excess of MAGI over: | |

| MFJ: $250,000 | Single: $200,000 |

| TAX CREDITS FOR CHILDREN | ||

|---|---|---|

| TYPE | AMOUNT | PHASEOUT RANGE |

| Child Tax Credit (Under 17) | $2,200 ($1,700 refundable) | Begins at $200,000 (single) Begins at $400,000 (MFJ) |

| Child and Dependent Care | 20-50% of the first $3,000 in qualified expenses (or the first $6,000 if you have 2 or more children) |

| STANDARD DEDUCTION | |

|---|---|

| FILING STATUS | ADDITIONAL (AGE 65/O) |

| MFJ | $32,200 Married (Each Eligible Spouse) $1,650 |

| Single | $16,100 Unmarried (Single, HOH) $2,050 |

| ITEMIZED DEDUCTIONS (SCHEDULE A) | ||

|---|---|---|

| TYPE | AMOUNT | PHASEOUT RANGE |

| SALT | $10,000 - $40,400 | $505,000 - $605,000 (single or MFJ) |

| NON-ITEMIZED BELOW-THE-LINE DEDUCTIONS | ||

|---|---|---|

| TYPE | AMOUNT | PHASEOUT RANGE |

| Senior (65+) | $6,000 (per eligible individual) | $75,000 - $175,000 (single) $150,000 - $250,000 (MFJ) |

| Charitable | $1,000 (single) $2,000 (MFJ) | N/A |

| Overtime | $12,500 (single) $25,000 (MFJ) | $150,000 - $275,000 (single) $300,000 - $550,000 (MFJ) |

| Tips | $25,000 (single or MFJ) | $150,000 - $400,000 (single) $300,000 - $550,000 (MFJ) |

| Car Loan Interest | $10,000 (on US-assembled vehicles) | $100,000 - $150,000 (single) $200,000 - $250,000 (MFJ) |

| QBI | Up to 20% of QBI ($400 minimum) | $201,750 - $276,750 (single)2 $403,500 - $553,500 (MFJ)2 |

| TAX CREDITS & DEDUCTIONS FOR EDUCATION | ||

|---|---|---|

| TYPE | AMOUNT | PHASEOUT RANGE |

| American Opportunity | 100% (first $2,000) 25% (next $2,000) | $80,000 - $90,000 (single) $160,000 - $180,000 (MFJ) |

| Lifetime Learning | 20% (first $10,000) | $80,000 - $90,000 (single) $160,000 - $180,000 (MFJ) |

| Student Loan Interest | $2,500 | $85,000 - $100,000 (single) $175,000 - $205,000 (MFJ) |

| ESTATE & GIFT TAX | ||

|---|---|---|

| LIFETIME EXEMPTION | TAX RATE | GIFT TAX ANNUAL EXCLUSION |

| $15,000,000 | 40% | $19,000 |

© fpPathfinder.com. Licensed for the sole use of Ben Smith of Cove Financial Planning, LLC. All rights reserved. Used with permission. Updated 11/26/2025.

From "The Owner's Almanac" - 90 days to build a business that runs without you. Available on Amazon.